Laying out the landscape for cash and investments in 2022 is like trying to skateboard during an earthquake. For those watching market predictions on how high or fast the Fed will raise rates in response to inflation and underlying economic conditions, the ground seems to be shifting at every turn.

Against a backdrop of two 25 basis point rate hikes by the Bank of England in December and February, and target rate probabilities for the March 16 Fed meeting changing in real time, treasury professionals tuned into ICD and BlackRock’s Global Markets Outlook webinar on February 10 to gain some perspective on money markets.

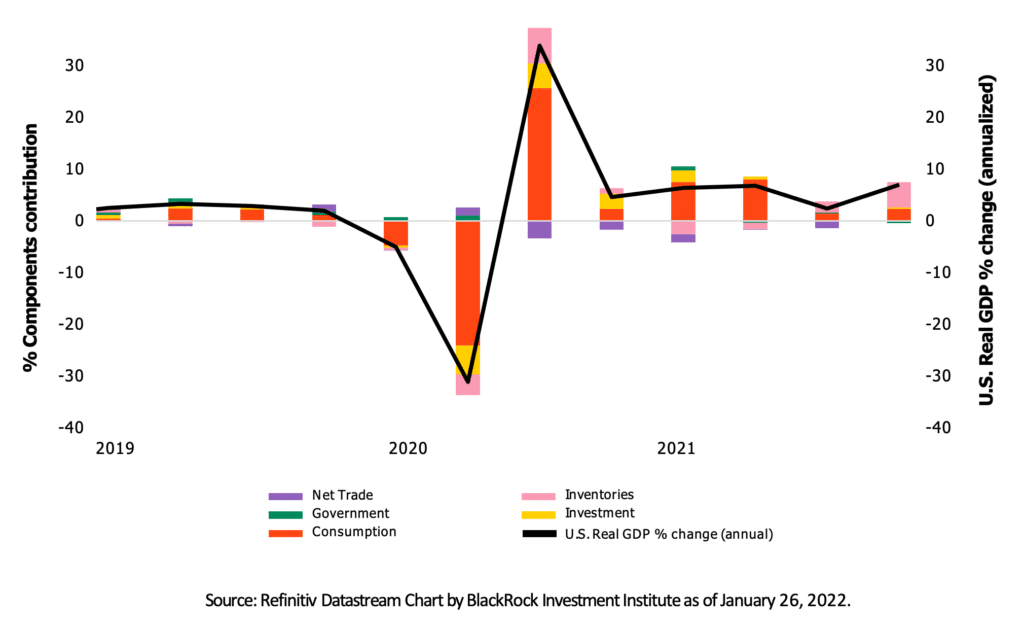

Rich Mejzak, BlackRock’s Head of Global Portfolio Management, Cash Management Group showed the relationship between the Fed’s “dual mandate” on inflation and employment, and trending GDP, the “advance” estimate of which was 6.9% at the time of the webinar.

Mr. Mejzak explained: “We’re, only expecting 1-1.5% growth in the first quarter of this year based partially on [inventory growth]. Is it an indication to some degree that the supply chain issues that we’ve been hearing about are in fact being repaired? A pickup in inventories would show that perhaps goods demand is flowing as well.”

In November last year, the Fed suggested we wipe our memories of the term ‘transitory’ when we think of inflation. Data released on the day of the webinar showed consumer prices in the U.S. pushed annual inflation up to 7.5%, the highest rate since 1982. The composition of GDP, and particularly inventories, will be something to watch, says Mr. Mejzak. “I would say this is one piece of evidence that, at least for right now, points in their direction.”

Looking ahead, BlackRock’s Eion D’Anjou, Portfolio Manager, US Government Funds, who joined Mr. Mejzak in the webinar, said: “We’re going to continue to see market volatility like we’re seeing today. It warrants being conservative with duration and maintaining above average liquidity.”

“Funds keep 50% seven days and shorter, so half your fund is going to benefit immediately from whatever that rake hike is,” Mr. Mejzak said. “What we’ve seen historically is, going forward, bank deposits are going to lag money funds in yield. What we hear is that banks are reluctant to get more deposits without the demand for loan growth on the other side.”

Treasury professionals in attendance seem to agree. About 70% polled said they were looking to maintain or reduce their investment levels in bank deposits.

Treasury teams should keep an eye on money market funds as rates change. ICD provides institutional investors with a daily yields and rates report and unbiased access to over 300 global funds, providing an expansive product selection to suit various investor requirements.