Unpacking the money markets in 2021 reveals a couple of truths in these uncertain times. First, cash is still king for institutional investors for the near term – even in this low-interest rate environment – and as the vaccine rolls out, so rolls the economy.

During an ICD webinar on April 20, Short-Term Investments in a Changing World, 58% of treasury professionals attending said they have no plans to reduce cash balances or are unsure about when they may see balances reduce to pre-Covid levels. This is in keeping with what ICD clients told us in January as 61% indicated that they expected to maintain or increase cash balances in the first half of 2021. The uncertainty driving cash balances is tied to the lingering effects of the pandemic’s initial shock, but there is some optimism looking out over the remainder of the year, especially as more people get vaccinated.

Thirty-six percent of treasury professionals attending the webinar said they foresaw their organizations reducing cash balances in the second half of the year, and even some (6%) said they were already at or below pre-Covid levels. This optimism also comes through the 68% of attendees that indicated they plan on resuming in-person business activity such as meetings, travel and conferences. Eighteen percent said they were ready to go now.

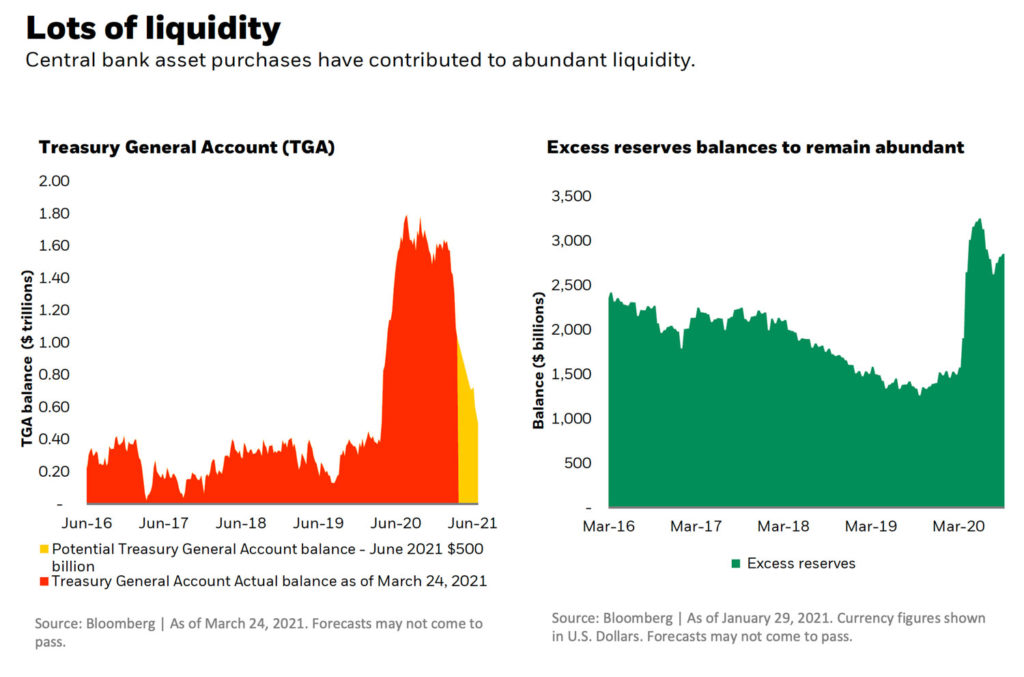

Thomas Kolimago, Global Head of Credit and Investment Research for Cash Management at BlackRock, who presented with ICD in the webinar, discussed the cash bubble created by the monetary and fiscal policies over the past year. Kolimago used the charts in Figure 1. to illustrate how cash will be flushed through the economy in the coming months. The charts demonstrate the nearly 1:1 correlation between activity in the Treasury’s “checking account” – the Treasury General Account (TGA) – and bank reserves.

Kolimago says:

Checks from the most recent COVID stimulus plan that went into effect this March went out to citizens very quickly. As that cash balance [from the TGA] starts to be drawn down, there’s this roughly one-to-one corresponding impact on excess reserves. So on the right, you see all that liquidity in the banking system, those excess reserve balances, which had already been rising as a result of the Fed’s asset repurchase program, jumped up as a result of the drawdown of the TGA balance.

These factors have caused so much liquidity in the system. Why that matters is that the increase in excess reserves from those two dynamics are putting downward pressure on money market rates. The outlook really is for that Treasury General Account to continue to be drawn down. Right now it’s around a trillion, and the Treasury’s expecting to draw that down to 500 billion. So more reserves will hit the system, and [the Fed] could even draw it down to around 100 billion in July, given the debt ceiling, due to certain statutory requirements. So this pressure at the front end is really likely to persist.

One tool the Fed uses in monetary policy is an administered rate, the interest on excess reserves rate [IOER], which is paid to banks keeping funds at the Fed. Will the IOER rate go up?

Concluding its two-day policy meeting on April 28, the Fed kept interest rates and its bond purchase program unchanged. That said, there are signs of the Fed’s concern over the glut of reserves in the system is having a downward effect on rates.

Kolimago explains:

The Fed’s not adopting, we believe, a negative policy rate regime. They’re loath to do that. We think that rates could still trade on Treasury bills and Repo in the negative levels. [The Fed] doesn’t want that to happen, we believe. But they have started to suggest, we’re watching this, and could adjust these administered rates as needed. So, I think it’s underscored the Fed’s aversion to negative rates. That’s a positive for money markets.